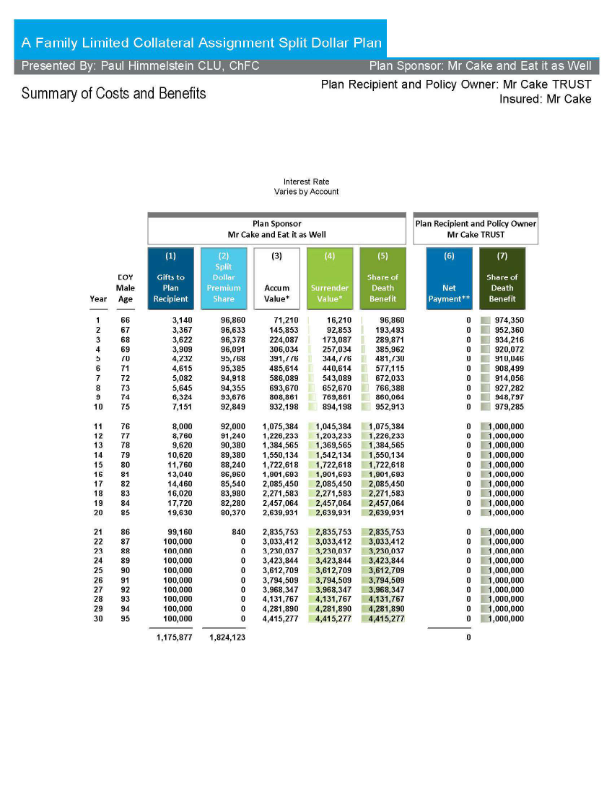

Here is the example: 65-Year-Old Male, STD NT

In this example, we used a 65-year-old male, standard-nonsmoker, and used an Indexed Universal Life (IUL) policy from a reputable company. In the first year, out of a $100,000 premium, the gift would only be $3,140 which controls 97% of the 1 million death benefit (i.e., $970,000). If that same client tried to purchase a one-year term life insurance policy with a $1 million death benefit, without conversion options and no commissions paid, the premium would be $5,421. For a 10-year term policy that can be converted, the premium would be $7,703. Thus, the $3,140 is substantially less expensive than buying the cheapest term policy, yet it offers a permanent solution.

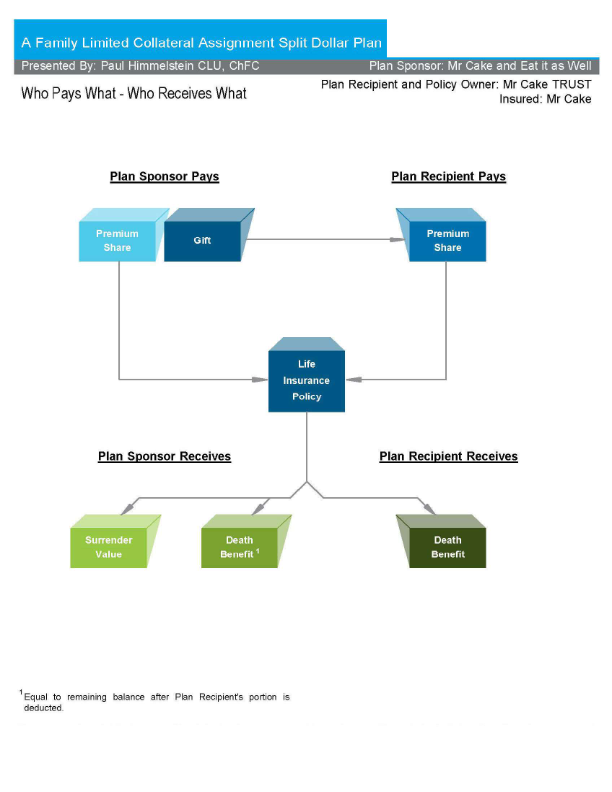

Additionally, note that the grantor has a lien on the contract (collateral assignment), which allows the grantor, trustee, or company head to maintain control of the excess funds. In the first year, 100% of the cash value is held by the grantor, company head if corporate, or individual spouse/trustee.

In the following flowchart, we illustrate how this arrangement works. The ledger example will be displayed underneath the flowchart. Please note that we can use different permanent products, including Whole Life (WL), Universal Life (UL), Indexed Universal Life (IUL), and Variable Universal Life (VUL). These options can be offered on a joint basis or an individual design.

To sum up the example, over 10 years, the client accumulates a value of $932,198, which is also the amount of the death benefit. The total cumulative gift over those 10 years is $47,087. In this scenario, the client would not have to report the gift as it is less than $17,000 per year for the first 10 years. At that time, there is total flexibility for the client’s trustee or, in a corporate situation, an officer, to choose whether to take back some or all of the money, re-gift that money, or continue with the original arrangement. The agreement can allow for all parties to receive their share, or the company can forgive the reimbursement in an employer-employee relationship. Additionally, the death benefit provides sufficient funds to cover these arrangements.